Does Home insurance cover water damage cleaning is an important question for many homeowners after a sudden leak, burst pipe, or appliance overflow. Finding water on your floor, walls, or carpet can feel stressful fast. You may worry about mold, repair costs, ruined furniture, and whether the cleanup company will cost more than you can afford. In many real water damage situations, homeowners do not just ask, “Is the damage covered?” They ask, “Will my insurance pay for water removal, drying, cleaning, and restoration?”

From reviewing common homeowners insurance water damage rules and cleanup claim situations, one thing is clear: the source of the water matters most. Home insurance may cover water damage cleaning if the damage is sudden, accidental, and caused by a covered event in your policy. But it usually does not cover floods, long-term leaks, poor maintenance, or sewer backups without extra coverage. This guide explains what may be covered, what is usually excluded, and what steps can help protect your claim.

Key Takeaways

Home insurance may cover water damage cleaning when the damage is sudden and accidental.

Covered cleanup may include water extraction, drying, sanitizing, damaged material removal, mold prevention, and repairs to covered property.

Flood cleanup is usually not covered by standard home insurance.

Sewer backup and sump pump overflow usually need extra coverage.

Mold cleanup may be covered if the mold resulted from a covered water damage event.

Insurance may pay for temporary housing if covered water damage makes your home unsafe to live in.

You should take photos, save receipts, contact your insurer quickly, and keep damaged items until they are documented.

If your claim is denied, review the denial letter and compare it with your policy.

What Is Water Damage Insurance?

Water damage insurance is not usually a separate policy. It is part of many homeowners insurance policies and may help pay for damage caused by certain water problems inside the home.

For example, a pipe may burst and soak your flooring. A washing machine hose may break and flood a laundry room. A water heater may suddenly leak and damage nearby walls.

In these situations, your policy may help pay for cleanup, drying, damaged material removal, and repairs.

However, insurance does not cover every water problem. Most policies cover sudden and accidental water damage, not damage that happens slowly over time.

Understanding Water Damage Insurance

Insurance companies look closely at the cause of the water damage before approving a claim.

They may ask:

- Where did the water come from?

- Was the damage sudden or gradual?

- Was the damage accidental?

- Could the problem have been prevented?

- Did the homeowner act quickly to reduce further damage?

A sudden event is more likely to be covered. A long-term problem is more likely to be denied.

For example, a pipe that bursts without warning may be covered. But a pipe that leaks under a sink for months may not be covered because the insurer may consider it a maintenance issue.

This is why the source and timing of the water damage matter so much.

Homeowners Insurance and Water Damage Coverage

Homeowners insurance may help pay for water damage cleaning if the cause of the damage is covered by your policy.

Covered services may include:

- Water extraction

- Drying wet areas

- Removing damaged drywall

- Removing wet carpet or padding

- Cleaning and sanitizing

- Mold prevention

- Odor control

- Repairing damaged floors or walls

- Cleaning damaged personal belongings

- Temporary repairs to prevent more damage

Your policy may also include limits and deductibles. A deductible is the amount you pay out of pocket before insurance starts paying for a covered claim.

Dwelling Coverage

Dwelling coverage protects the structure of your home.

This may include:

- Walls

- Floors

- Ceilings

- Built-in cabinets

- Plumbing systems

- Roof

- Attached structures

If a covered water event damages your home, dwelling coverage may help pay for cleanup and repairs.

For example, if a pipe bursts inside a wall and damages drywall, flooring, insulation, and paint, dwelling coverage may help pay for drying, damaged material removal, and repair work.

However, your policy may not pay to repair or replace the item that caused the damage. For example, it may cover the water damage from a broken pipe but not the cost of replacing the pipe itself.

Personal Property Coverage

Personal property coverage protects your belongings.

This may include:

- Furniture

- Clothing

- Electronics

- Rugs

- Books

- Small appliances

- Personal items

If a covered water event damages your belongings, your policy may help pay to clean, repair, or replace them.

For example, if a burst pipe soaks your sofa, rug, and electronics, personal property coverage may help cover those losses.

However, some items may have limits. Expensive jewelry, collectibles, artwork, or electronics may need extra coverage.

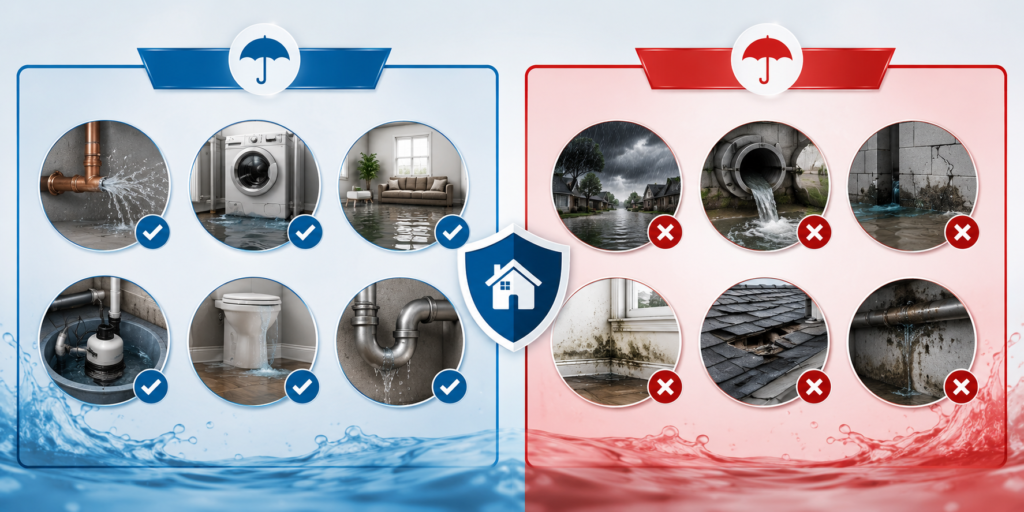

What Types of Water Damage Are Covered?

Home insurance often covers sudden and accidental water damage.

Common covered examples may include:

- Burst pipes

- Broken appliance hoses

- Sudden water heater leaks

- Accidental toilet overflow

- Accidental sink or bathtub overflow

- Water damage from a covered roof leak

- Fire sprinkler water damage

- Water used to put out a fire

- Sudden HVAC or appliance-related leaks

These events usually happen quickly and are not caused by neglect. That is why they may be covered.

Still, every policy is different. Always check your policy or ask your insurance company before assuming coverage.

Does Home Insurance Cover Water Damage Cleaning?

Yes, home insurance may cover water damage cleaning if the water damage itself is covered by your policy.

This means the cleanup must be connected to a covered event.

For example, if a pipe bursts and water floods your living room, your policy may pay for water removal, drying equipment, damaged flooring removal, drywall repair, and sanitizing.

Covered water damage cleaning may include:

- Removing standing water

- Drying walls, floors, and furniture

- Using fans and dehumidifiers

- Cleaning wet surfaces

- Removing damaged materials

- Preventing mold growth

- Sanitizing affected areas

- Cleaning damaged belongings

- Repairing damaged parts of the home

The cleanup must be reasonable and necessary. Your insurance company may review the restoration bill before paying.

What Should You Do Right Away After Water Damage?

If water damage is happening now, your first goal is to stop more damage.

Follow these steps:

- Stop the water source if it is safe.

- Move people and pets away from unsafe areas.

- Turn off electricity in wet areas if needed.

- Take photos and videos before cleanup.

- Call your insurance company.

- Ask what emergency cleanup is approved.

- Start reasonable cleanup to prevent further damage.

- Keep damaged items until they are documented.

- Save every receipt and invoice.

Do not wait too long. Wet walls, flooring, and furniture can lead to mold, odors, structural damage, and higher repair costs.

What Water Damage Cleaning Costs May Insurance Cover?

If the water damage is covered, your policy may help pay for reasonable cleanup costs.

These costs may include water extraction, drying equipment, labor, removing wet materials, sanitizing, odor control, mold prevention, debris removal, and repairs to damaged parts of the home.

Common covered cleaning costs may include:

- Emergency water removal

- Professional drying

- Air movers and dehumidifiers

- Moisture testing

- Removing wet carpet or padding

- Removing damaged drywall

- Cleaning hard surfaces

- Sanitizing affected areas

- Debris removal

- Mold prevention

- Cleaning damaged belongings

- Temporary repairs

Your insurer may review the cleanup bill before paying. You may also need to pay your deductible first.

Insurance usually does not pay for upgrades, unrelated repairs, or damage caused by neglect.

What If You Already Have a Cleanup Bill?

If you already have a bill from a water damage restoration company, do not ignore it.

Ask the company for an itemized invoice. The invoice should clearly show what work was done, when it was done, and why it was needed.

A good cleanup bill may include:

- Date of service

- Cause of water damage

- Rooms affected

- Equipment used

- Labor hours

- Materials removed

- Moisture readings

- Photos, if available

- Drying logs, if available

Send the invoice to your insurance company or adjuster as soon as possible.

Insurance may not pay every charge, but clear records can help support your claim.

Covered vs. Not Covered Water Damage Cleaning

Here is a simple guide to common water damage cleaning situations.

| Water damage cleaning situation | Usually covered? | Reason |

| Burst pipe cleanup | Yes | Sudden and accidental |

| Washing machine hose leak cleanup | Yes | Sudden appliance failure |

| Water heater rupture cleanup | Yes | Sudden internal water damage |

| Toilet overflow cleanup | Often yes | If accidental |

| Roof leak cleanup after storm damage | Often yes | If storm damage is covered |

| Slow pipe leak cleanup | Usually no | Gradual damage |

| Flood cleanup | No | Needs flood insurance |

| Sewer backup cleanup | Usually no | Needs extra water backup coverage |

| Sump pump failure cleanup | Usually no | May need an endorsement |

| Mold cleanup | Sometimes | Depends on the cause and policy limits |

This table is only a general guide. Your final coverage depends on your policy.

Does Homeowners Insurance Cover Water Damage From Leaking Plumbing?

Homeowners insurance may cover water damage from leaking plumbing if the leak is sudden and accidental.

For example, a pipe may burst in cold weather, a supply line may suddenly break, or a toilet may overflow by accident. These events may be covered.

But a slow leak is different. If a pipe leaks for weeks or months, the damage may not be covered because the insurer may consider it a maintenance issue.

The answer depends on how the leak happened and whether the homeowner acted reasonably after discovering it.

What Types of Water Damage Are Not Covered?

Many types of water damage are not covered by a standard home insurance policy.

Common exclusions include:

- Flood damage

- Groundwater seepage

- Sewer backup without extra coverage

- Sump pump failure without extra coverage

- Long-term leaks

- Poor maintenance

- Mold from neglect

- Water damage from humidity

- Water damage from normal wear and tear

- Damage from ignored roof or plumbing problems

These problems are often considered preventable or outside the basic policy.

This is why it is important to understand your coverage before water damage happens.

Damage From Unresolved Maintenance Issues

Home insurance usually does not cover damage caused by poor maintenance.

For example, if you notice a small leak under your sink and ignore it for months, it may cause mold, damaged cabinets, and flooring problems.

Your insurance company may deny the claim because the damage was not sudden.

The same can happen with old roofs, broken seals, clogged gutters, damaged plumbing, or appliances that were not maintained.

To avoid this problem, fix small issues early and keep records of repairs.

Replacing or Repairing the Source of the Water Damage

Home insurance may cover the damage caused by water, but it may not cover the item that caused the damage.

For example, your water heater may burst and damage the floor. Insurance may pay to repair the floor, but it may not pay to replace the old water heater.

The same may apply to a broken pipe, appliance, roof part, or plumbing fixture.

This is an important point because many homeowners think insurance will pay for everything. In many cases, insurance only pays for the resulting damage, not the failed item itself.

Water Backup From an Outside Sewer or Drain

Standard home insurance usually does not cover sewer backup cleanup unless you have water backup or sewer backup coverage.

This type of damage can be expensive and may require special cleaning because the water may be contaminated.

Sewer backup cleanup may include:

- Removing dirty water

- Sanitizing floors and walls

- Removing damaged materials

- Odor control

- Mold prevention

- Cleaning personal items

- Professional disinfection

You may need a water backup endorsement for this type of claim.

An endorsement is extra coverage added to your policy.

Flood

Standard home insurance usually does not cover flood damage.

A flood is water that comes from outside and enters your home. This may happen because of:

- Heavy rain

- Rising rivers

- Storm surge

- Overflowing lakes

- Surface water

- Groundwater

If floodwater enters your home, standard home insurance will likely not pay for cleanup.

You usually need a separate flood insurance policy for flood damage.

This is especially important for homeowners in flood-prone areas.

How Can You Tell If Basement Water Is Covered?

Basement water can be confusing because the source matters.

If a pipe bursts in the basement, cleanup may be covered. If a water heater suddenly ruptures, cleanup may also be covered.

But if rainwater enters from outside, it may count as floodwater or seepage. Standard home insurance usually does not cover that.

If a sump pump fails, you may need sump pump or water backup coverage.

If sewage comes up through a drain, you may need sewer backup coverage.

Before filing a claim, try to identify where the water came from. Photos, plumber reports, and restoration company notes may help prove the cause.

Does the Type of Water Affect Cleanup?

Yes, the type of water can affect cleanup, cost, safety, and insurance coverage.

Clean water from a broken pipe is different from dirty water from a sewer backup or flood. Dirty or contaminated water may require special equipment, protective gear, sanitizing, and professional cleanup.

There are three common types of water damage:

Clean Water

Clean water may come from a broken supply line, burst pipe, or leaking clean water appliance line.

It is usually less dangerous than dirty water, but it can still damage walls, floors, furniture, insulation, and personal belongings.

Clean water can also lead to mold if the area is not dried quickly.

Gray Water

Gray water may come from appliances, sinks, dishwashers, or washing machines.

It may contain dirt, soap, food particles, or other waste.

Gray water usually needs stronger cleaning and sanitizing than clean water.

Black Water

Black water is unsafe and contaminated water. It may come from sewage, floodwater, stormwater, or other polluted sources.

Black water cleanup may require professional help, special equipment, sanitizing, and removal of contaminated materials.

It may also affect your insurance claim because sewer backup and floodwater often require extra coverage.

Water Damage Claims and Costs

Water damage cleaning can be expensive. The total cost depends on the size of the damage, the type of water, the rooms affected, and how long the water sat before cleanup started.

Costs may include:

- Emergency water removal

- Drying equipment

- Labor

- Moisture testing

- Demolition

- Mold prevention

- Sanitizing

- Repairs

- Personal property cleaning

- Temporary housing

Your insurance company may send an adjuster to inspect the damage. The adjuster reviews the cause, the damage, photos, invoices, and cleanup costs.

Then the company decides what is covered under your policy.

Types of Water Damage Claims

There are several common types of water damage claims.

Burst Pipe Claims

A burst pipe claim may be covered if the pipe broke suddenly. The policy may pay for cleanup, drying, damaged material removal, and repairs.

Appliance Leak Claims

A washing machine, dishwasher, refrigerator line, or water heater may suddenly leak. If the leak is accidental and sudden, cleanup may be covered.

Toilet Overflow Claims

A toilet overflow may be covered if it happens by accident. But it may not be covered if it was caused by neglect, repeated clogging, or sewer backup without extra coverage.

Roof Leak Claims

A roof leak may be covered if a covered event, such as wind or storm damage, caused the leak. But an old, worn, or poorly maintained roof may not be covered.

Sewer Backup Claims

Sewer backup is often not covered unless you have extra water backup or sewer backup coverage.

Flood Claims

Flood claims usually require separate flood insurance. Standard homeowners insurance usually does not cover flood cleanup.

How to File a Water Damage Claim

Act fast after water damage. This can help protect your home and your claim.

Follow these steps:

- Stop the water if it is safe.

- Turn off electricity in wet areas if needed.

- Take photos and videos before cleaning.

- Call your insurance company.

- Ask what emergency cleanup is approved.

- Call a water damage cleanup company if needed.

- Save all receipts and invoices.

- Keep damaged items until they are documented.

- Write down what happened.

- Get a plumber or restoration report if needed.

- Meet with the insurance adjuster.

- Review your claim payment.

- Pay your deductible.

Do not wait too long. Waiting can make the damage worse and may make your claim harder to prove.

Should You Clean Up Water Damage Before the Adjuster Comes?

Yes, you should take reasonable steps to prevent more damage. But document everything first.

Take clear photos and videos of the water source, damaged rooms, wet floors, damaged furniture, walls, ceilings, and any standing water.

Then you can start basic cleanup.

You may need to remove water, dry the space, or call a restoration company. This can help prevent mold and further damage.

However, do not throw away damaged items too soon. If you must throw something away for safety, take photos first.

You can make emergency repairs to stop more damage, but avoid major permanent repairs until your insurer has inspected the damage or approved the work.

Does Insurance Cover Water Mitigation?

Home insurance may cover water mitigation if the water damage is covered.

Water mitigation means stopping more damage from happening. It is not the same as full repair.

Water mitigation may include:

- Water extraction

- Drying wet areas

- Setting up fans

- Using dehumidifiers

- Removing wet carpet

- Removing damaged drywall

- Checking moisture levels

- Temporary repairs

- Tarping or sealing areas if needed

Insurance companies usually expect homeowners to take reasonable steps to prevent further damage after a loss. Because of that, mitigation can be an important part of the claim.

Still, you should contact your insurer quickly and ask what work is approved.

Does Insurance Cover Mold Cleanup After Water Damage?

Mold cleanup may be covered if the mold resulted from a covered water damage event and you acted quickly to prevent further damage.

For example, a pipe bursts while you are away for the day. Water soaks the wall, and mold begins to grow before the area is fully dried. In that case, your policy may help pay for mold cleanup.

But mold from long-term leaks, humidity, or neglect is usually not covered.

Mold may also have coverage limits. Some policies only pay a certain amount for mold removal.

To protect your claim, dry the area quickly, report the damage fast, and keep records of cleanup work.

Does Home Insurance Pay for Temporary Housing After Water Damage?

Home insurance may pay for temporary housing if covered water damage makes your home unsafe to live in.

This is often called loss of use coverage.

Loss of use coverage may help pay for extra living costs while your home is being repaired.

This may include:

- Hotel stays

- Short-term rentals

- Extra meal costs

- Laundry costs

- Pet boarding

- Other necessary living expenses

However, this coverage has limits. It also only applies if the damage is covered by your policy.

For example, if a covered burst pipe makes your home unsafe, loss of use coverage may help. But if flood damage is not covered by your policy, temporary housing may not be covered either.

What If Your Water Damage Claim Is Denied?

A water damage claim can be denied for several reasons.

Common reasons include:

- The damage came from a flood.

- The damage came from a slow leak.

- The damage was caused by poor maintenance.

- You did not have sewer backup coverage.

- You did not have sump pump coverage.

- You waited too long to report the claim.

- The insurer says the damage was not sudden.

- You did not have enough photos or records.

- The cleanup bill was not properly documented.

If your claim is denied, read the denial letter carefully. Then compare it with your policy.

You can also ask your insurer what evidence is missing. In some cases, a plumber’s report, restoration invoice, moisture readings, photos, or repair records may help support your claim.

Special Considerations

Water damage claims can be complex. Your policy may include limits, exclusions, deductibles, and special rules.

Before filing a claim, check these parts of your policy:

- Deductible

- Dwelling coverage limit

- Personal property coverage limit

- Water backup coverage

- Sump pump coverage

- Mold coverage limit

- Flood exclusion

- Loss of use coverage

- Replacement cost coverage

- Actual cash value coverage

You should also compare the repair cost with your deductible. If the damage is small and the cleanup cost is close to your deductible, it may not make sense to file a claim.

If you do not understand your policy, ask your insurance agent.

What Extra Coverage Can Help With Water Damage Cleaning?

Some water damage cleanup is not covered by a standard policy, but you may be able to add extra coverage.

Ask your insurance company about:

- Water backup coverage

- Sewer backup coverage

- Sump pump overflow coverage

- Flood insurance

- Mold coverage

- Service line coverage

- Replacement cost coverage

These options may help protect you from common water damage exclusions.

They can be especially useful for homeowners, condo owners, landlords, new buyers, and people living in areas with basements or flood risk.

What’s the Difference Between Actual Cash Value and Replacement Cost?

Actual cash value pays based on the item’s used value. It subtracts for age, wear, and depreciation.

Replacement cost pays to replace the item with a similar new item. It usually does not subtract as much for age.

For example, if your old sofa is damaged by water, actual cash value may pay less because the sofa was used. Replacement cost may pay more because it helps you buy a similar new sofa.

Your policy will say which type of coverage you have.

What If You Are a Condo Owner or Landlord?

Water damage coverage can be different for condo owners and landlords.

If you own a condo, your personal condo policy may cover your unit, belongings, and improvements. But the condo association’s master policy may cover shared areas or parts of the building structure.

If you are a landlord, your landlord policy may cover the rental building. But it usually does not cover your tenant’s personal belongings. Tenants usually need renters insurance for their own property.

In both cases, the cause of the water damage still matters.

Condo owners should check their condo policy and HOA master policy. Landlords should check their landlord insurance policy and encourage tenants to carry renters insurance.

Conclusion

After reviewing how homeowners insurance usually handles water damage claims, the main point is clear: the cause of the water damage matters most. Home insurance may cover water damage cleaning if the damage was sudden, accidental, and covered by your policy, such as a burst pipe or appliance leak. But cleanup from floods, long-term leaks, poor maintenance, sewer backup, or sump pump failure may not be covered without extra coverage. In real claim situations, fast action and strong proof can help a lot. Take photos before cleaning, stop the water if it is safe, call your insurer quickly, and save every receipt. Your final payout will depend on your policy terms, limits, deductible, endorsements, and exclusions.

FAQ

Does homeowners insurance cover water damage cleanup?

Yes, it may cover water damage cleanup if the damage was sudden, accidental, and caused by a covered event.

Does insurance cover water extraction?

Insurance may cover water extraction if it is needed after a covered water damage claim

Does insurance cover cleanup after a burst pipe?

Yes, cleanup after a burst pipe is often covered if the pipe broke suddenly and the damage was not caused by neglect.

Does homeowners insurance cover sewage cleanup?

Usually not under a standard policy. You may need sewer backup or water backup coverage.

Does home insurance cover flood cleanup?

No, standard home insurance usually does not cover flood cleanup. You normally need separate flood insurance.

Does insurance cover mold cleanup after water damage?

It may cover mold cleanup if the mold came from a covered water damage event and you acted quickly.

Should I clean up water damage before the adjuster comes?

Yes, but take photos and videos first. Then make reasonable cleanup efforts to prevent more damage.

Can my water damage claim be denied?

Yes. Claims may be denied for flood damage, slow leaks, poor maintenance, missing coverage, or late reporting.

Does home insurance cover roof leak water damage?

It may cover roof leak water damage if the leak was caused by a covered event, such as storm damage.

How long do I have to file a water damage claim?

The deadline depends on your insurer and policy. It is best to report water damage as soon as possible.